Care and Maintenance

Long Handle Squeegee: Your Ultimate Guide to Pro Results

Master high-reach window cleaning with our guide to the long handle squeegee. Learn to choose the right size, use proper technique, and get streak-free results.

When you're looking at a service contract, the terms bonded and insured can feel like confusing jargon. But they're two of the most important words you'll see. It's crucial to understand what they mean for your protection.

Let's break it down. Being insured protects the contractor’s business if an accident happens on your property. Being bonded, on the other hand, protects you—the client—if the work isn't finished or if something shady occurs, like theft. A company that has both is the one you can trust.

Think of it this way: insurance is for the "what ifs," like a ladder accidentally falling through your window. A bond is a promise that the job you’re paying for will actually get done, and done honestly.

For any homeowner hiring a pro—whether it's for window cleaning in Phoenix or a major renovation in Denver—getting this difference is the first step toward a secure, worry-free project.

At Professional Window Cleaning, we’ve built our reputation on being completely transparent and protecting our clients. Professional Window Cleaning has been cleaning windows for over 26 years! We want you to feel confident in your hiring decisions, so let’s unpack exactly what these protections mean.

To make this crystal clear, let's put these two protections side-by-side. This table breaks down the core distinctions so you can see exactly who and what is covered.

| Aspect | Bonded | Insured |

|---|---|---|

| Who It Protects | The client (you) from financial loss. | The business from financial liability. |

| What It Covers | Theft, dishonesty, or failure to complete the work. | Accidents, property damage, and injuries. |

| Primary Purpose | Guarantees contractual obligations are met. | Covers operational risks and mishaps. |

| Claim Payout | The surety company pays you, then seeks reimbursement from the contractor. | The insurance company pays for covered losses without seeking reimbursement from the contractor. |

Seeing them compared like this makes it easy to understand why both are so important for your peace of mind.

Key Takeaway: A bond is a promise backed by a third party that the job will be done ethically and completely. Insurance is a safety net for when accidents happen during the job.

Hiring a contractor who is both bonded and insured isn't just a good idea; it’s a non-negotiable step to protect your home and your investment. It shows that a contractor is serious about their work, committed to professionalism, and financially accountable. You're covered from every angle, whether you live in Las Vegas or Scottsdale.

You’ve probably heard a contractor say they're "fully insured." While it sounds great, what does that really mean for you and your property? It’s not just a catchphrase; it’s a critical shield for your finances, built on two key policies: General Liability Insurance and Workers' Compensation Insurance.

Knowing the difference is the first step in protecting yourself. One covers your property, and the other covers you from liability if a worker gets hurt. Let's break down what each one does.

Think of General Liability as your primary defense against property damage and accidents. It's designed to pay for mishaps caused by a contractor's work, so you aren't left holding the bill or, even worse, filing a claim on your own homeowner's policy.

Imagine a window cleaning technician is working on your beautiful home in Scottsdale and accidentally drops a tool, cracking a large, custom picture window. This is exactly where their General Liability insurance springs into action.

This kind of scenario is precisely why verifying a contractor's insurance is a non-negotiable step. It effectively transfers the financial risk from your shoulders to their insurer. It’s a core part of the professionalism we’ve brought to every job for over 26 years.

While General Liability protects your property, Workers' Compensation protects you if a contractor’s employee is injured on your property. This is a critical detail that homeowners and property managers in places like Phoenix can't afford to overlook.

Here’s a tough but realistic situation: a technician from an uninsured company falls from a ladder while cleaning your second-story windows. Without Workers' Comp, you could be held personally liable for their medical bills, lost wages, and long-term care. That single accident could lead to a financially devastating lawsuit.

A contractor’s Workers' Compensation policy ensures their team is covered for any work-related injuries, taking you completely out of the picture. It's an absolute must-have that shields you from massive legal and financial risk.

Before you let anyone start work, always ask for their Certificate of Insurance (COI). This document is the ultimate proof that a contractor holds active General Liability and Workers' Compensation policies. Any truly professional company will provide it without a second thought because they know it’s about protecting you.

While contractor insurance covers accidents, a surety bond is what truly protects your investment. Think of it less like insurance for the contractor and more like a financial guarantee for you, the client. It’s all about making sure the contractor upholds their end of the deal.

So, how does it work? A surety bond is a three-way pact between:

This setup creates a powerful layer of accountability. If your contractor doesn't follow through, the surety company is obligated to step in and help make things right for you. Our clients in cities like Denver and Phoenix know this protection is key.

For homeowners and property managers, two kinds of bonds are absolutely critical: performance bonds and fidelity bonds. Each one tackles a different kind of risk, giving you peace of mind from multiple angles.

A performance bond guarantees the job you paid for will actually get done. Let’s say you hire a company for a major window cleaning project on a Las Vegas high-rise and put down a hefty deposit. If they suddenly disappear or just fail to do the work, you can file a claim against their bond to get your money back.

A fidelity bond is your protection against dishonesty or theft. If an employee from the service company steals from your property while on the job, the fidelity bond is your pathway to being compensated for that loss.

A surety bond essentially forces a contractor to be accountable. It’s a formal guarantee of professionalism and financial integrity, demonstrating that a third-party financial institution has vetted the contractor and trusts them to fulfill their promises.

This is the key difference between being bonded and insured. Insurance pays for accidents, but a bond ensures the contractor is ultimately on the hook for their failures. The contractor has to reimburse the surety for any claims paid out, which is a massive incentive to do the job right. You can find more great insights on this topic over at Westfield Insurance's blog.

When you hire a company like Professional Window Cleaning—which has proudly served clients across Arizona, Colorado, and Nevada for over 26 years—our bond means we back our work with more than just a handshake. It's a solid financial promise that your project will be completed with absolute integrity.

It's one thing to know the dictionary definitions of "bonded" and "insured," but it’s another to see how they actually protect you when things go sideways. This is where the theory meets the real world of property management and home ownership.

Let's walk through a few scenarios that show exactly how bond and insurance claims work in practice. The core difference is simple but powerful: Insurance covers operational mishaps, while bonds cover contractual promises. Understanding this distinction is everything when it comes to protecting your investment.

Imagine our window cleaning crew is using a professional pure-water system at a high-end car dealership you manage in Las Vegas. In professional window cleaning, there are only two methods used: a squeegee and a pure-water system. Suddenly, a hose connection on the pure-water system bursts, spraying water inside the showroom and soaking the leather interior of a brand-new luxury vehicle.

This is a textbook insurance claim. Here’s the play-by-play:

Now, let's look at a completely different kind of problem. Suppose you hire a company to clean the windows of a new high-rise stadium in Denver right before its grand opening. You pay a hefty deposit, but the company never shows up, leaving you in a serious bind with a tight deadline looming.

This is exactly why surety bonds exist. A bond claim is your safety net here.

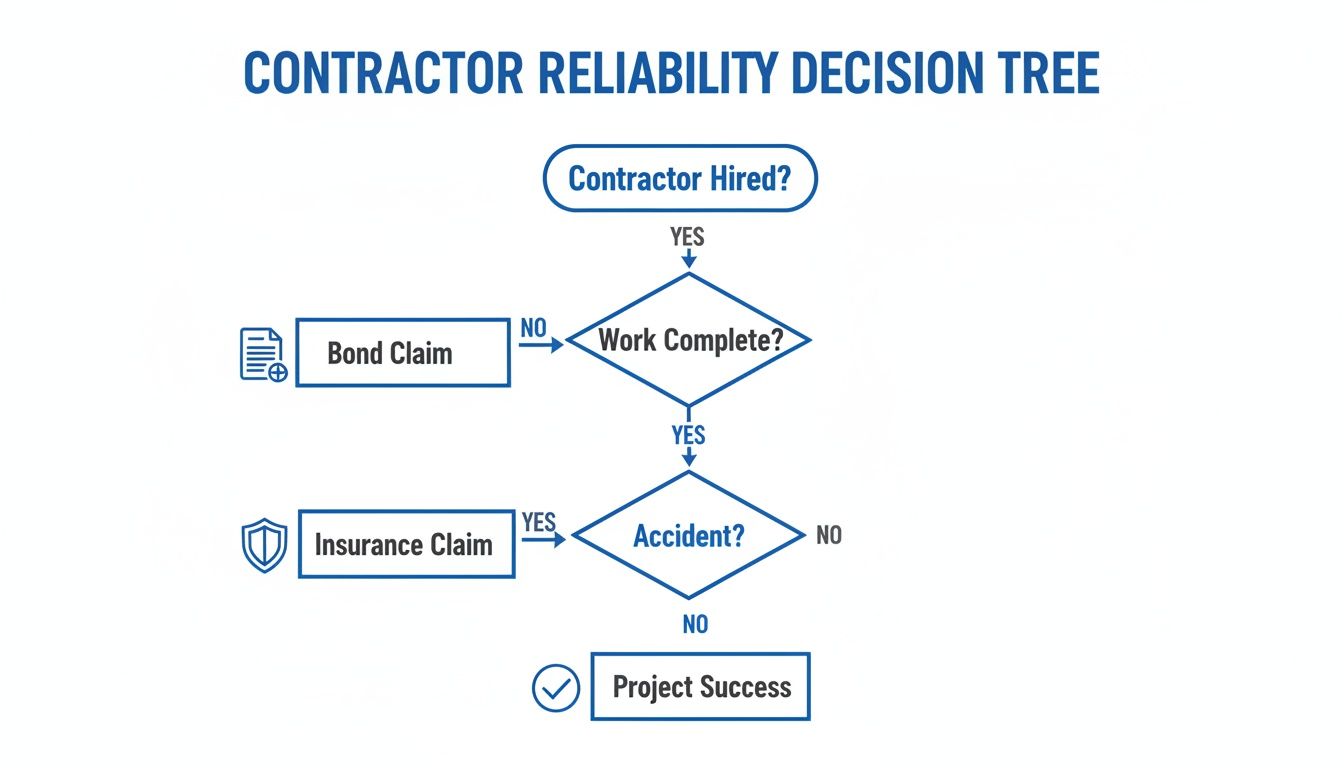

The decision tree below gives you a quick visual guide for when a bond claim is the right move versus an insurance claim.

As you can see, the path is clear: bond claims are for failures related to the work itself, while insurance claims are for accidents that happen during the work.

To give you an idea of how crucial this is, the surety bond market once paid out a staggering $1.3 billion in contract surety claims in a single year. That figure, from a Surety & Fidelity Association of America report, shows just how often bonds are the mechanism that saves project owners when contractors don't deliver. It’s a vital tool that transfers risk from your shoulders to the surety company.

To break it down even further, think of it this way: insurance is for "oops," while a bond is for "I promise." This table shows how they stack up side-by-side from your perspective as the client.

| Protection Aspect | Surety Bond (Bonded) | Liability Insurance (Insured) |

|---|---|---|

| Primary Purpose | Guarantees the contractor will fulfill their contractual obligations (e.g., finish the job, pay subcontractors). | Covers accidental damage, injuries, or negligence that occurs while the contractor is working. |

| Who is Protected? | You, the client. It protects you from financial loss if the contractor fails to perform. | The contractor's business. It protects them from having to pay for damages out-of-pocket, which indirectly protects you. |

| Claim Trigger | The contractor breaks the terms of the contract (e.g., non-completion, theft, not paying suppliers). | An accident happens (e.g., property damage, bodily injury to a third party). |

| Payout Source | The surety company pays you, then seeks reimbursement from the contractor. | The insurance company pays for the covered damages or liability claims. |

| Example Scenario | A hired painter takes your deposit and never returns to finish the job. | A painter accidentally spills a can of paint on your expensive hardwood floors. |

| Financial Nature | A form of credit. The contractor pays a premium, but the surety expects to be paid back if a claim is paid. | A risk transfer tool. The contractor pays premiums to transfer the risk of accidents to the insurer. |

Both of these protections work together to create a complete safety net for you. One without the other leaves a major gap in your protection.

A key takeaway: Bond and insurance protections are not interchangeable. They are complementary safeguards that every reputable company, like Professional Window Cleaning with its 26+ years of experience in cities like Phoenix, should carry to offer complete client protection.

Hiring a contractor who is both bonded and insured means you’re covered whether a window is accidentally shattered or the entire job is left unfinished. It is the only way to get total peace of mind and ensure you’re never left holding the bag.

Any contractor can say they’re bonded and insured, but the real proof is always in the paperwork. A reputable company won't just tell you—they'll show you, proactively offering up their credentials as a normal part of doing business. Taking just a few minutes to check this information is the single best thing you can do to protect your property and your wallet.

Don’t just take their word for it. This simple act of due diligence is what separates the true professionals from the risky hires. For a company like Professional Window Cleaning, with over 26 years of integrity, providing this documentation is just how we earn your trust from day one.

Before any work kicks off, there are two key documents you need to ask for and review. These are the official proof that a contractor has the coverage they claim.

Any legitimate contractor will have these ready to go and will be happy to share them. If you get any hesitation or an outright refusal, consider it a major red flag. This verification step is vital whether you're hiring for window cleaning in Scottsdale or another trade; for instance, knowing how to choose the right landscaping contractor involves the exact same steps to check their professional safeguards.

Once you have the paperwork, you need to know what you're looking at. The details are everything—an expired policy or weak coverage limits offer you zero protection.

On the Certificate of Insurance, you’ll want to check these key details:

For the Surety Bond, look for the name of the surety company and the bond number. But the most important step comes next: independent verification.

Pro Tip: Never rely only on the piece of paper a contractor hands you. Always take five minutes to call the insurance agent and the surety company listed on the documents. Ask them to confirm the policies are active and in good standing. This quick call gives you absolute peace of mind.

This final step ensures the documents haven't been faked or altered. By following through, you confirm that the contractor's promises are backed by real, verifiable protection for your home or business in areas we service, like Phoenix and Las Vegas. If you're looking for other ways to make professional services work for your budget, you might find our guide on finding affordable window cleaning near you helpful.

So, after breaking down the details, what’s the final verdict? It’s simple: for complete peace of mind, homeowners and property managers should only hire contractors who are both bonded and insured.

Choosing a pro with one but not the other is like locking your front door but leaving the back door wide open. You're leaving yourself exposed, because these two protections solve entirely different problems.

Think of it as the ultimate safety net for your property. You aren't just getting one layer of protection—you're covering two completely separate kinds of risk:

Choosing a bonded and insured company means you're partnering with a business committed to professionalism, accountability, and excellence. It’s the gold standard for consumer protection.

It’s a standard we've lived by at Professional Window Cleaning for over 26 years. It's how we protect our clients, from residential homes in Scottsdale to sprawling commercial properties in Denver. This comprehensive approach ensures that no matter what happens, your project and investment are secure.

Wondering how these essential protections factor into the overall price? We break it down in our guide on understanding cleaning services cost. Ultimately, making sure your contractor is both bonded and insured isn't just a smart move—it’s a non-negotiable for a worry-free experience.

It's easy to get tangled in the web of contractor jargon. When you're trying to make a smart hiring decision, terms like "licensed," "bonded," and "insured" can feel overwhelming. Let's clear things up with direct answers to the questions we hear most from homeowners and property managers in places like Phoenix, Scottsdale, Las Vegas, and Denver.

Not at all—these are three completely separate credentials, and each one protects you in a different way. A license is simply the government's permission for a contractor to legally offer their trade in a state or city. Think of it as passing the driver's test.

Being bonded and insured, on the other hand, are financial safety nets. They prove a contractor has the financial backing to make things right if something goes wrong. A license proves they can do the work, but bonds and insurance prove they're financially responsible.

This is a scenario no homeowner wants to imagine. If you hire a contractor who doesn't carry their own Workers' Compensation insurance, and one of their employees gets injured on your property, you could be held personally liable for all of it—their medical bills, lost wages, and more. It's a massive financial risk that can easily spiral into a costly lawsuit against you.

That’s why verifying a contractor's Workers' Comp policy is absolutely non-negotiable before anyone sets foot on your property to start work.

Key Insight: The absence of a contractor's insurance doesn't eliminate risk—it transfers it directly to you. A professional company carries proper coverage to protect both their team and their clients.

It really depends on the bond's specific terms. A performance bond is designed to protect you if a contractor takes your money and fails to complete the job as spelled out in your agreement.

While it might cover work that is so shoddy it’s essentially incomplete, it typically doesn't cover minor complaints about aesthetics. For example, if your window cleaning crew leaves an entire floor of windows untouched, a bond claim might be appropriate. But if you find a few minor streaks, that's something you’d handle directly with the company. Professional Window Cleaning has been cleaning windows for over 26 years, and we guarantee your satisfaction.

Simply put, it costs money. Obtaining bonds and insurance requires a business to be financially stable with a proven track record. Some contractors skip these crucial steps to slash their overhead and offer rock-bottom prices, but that lower price comes at a huge risk to you, the client.

A company's investment in being fully bonded and insured is one of the clearest signals of their professionalism, stability, and long-term commitment to their customers. For property managers who have more questions about overseeing larger projects, this common query is a great resource: Do You Oversee Remodels And Construction Projects.

For total peace of mind on your next window cleaning project in Phoenix, Denver, or Las Vegas, trust the team that has been fully bonded and insured for over 26 years. Contact Professional Window Cleaning for a free, no-obligation estimate today! https://www.professionalwindowcleaning.com

Read our blog posts regularly and keep learning.